UPDATE 06/02/2023 — Allstate and Farmers join State Farm in denying new homeowner policies in California. State Farm quit selling new homeowner policies on Saturday, and now a second major carrier, Allstate Insurance, has confirmed it ended new homeowners’ policies in the state last year. On top of that, ABC-7 News reported that Farmers Insurance is now limiting policies for new customers. All three companies are still serving existing customers, and more than 100 other companies are still issuing new homeowners’ policies, but homeowners across the state will have a tougher time buying coverage.

State Farm will no longer provide home insurance to new California customers because of wildfire risks and increased construction costs. The company quit accepting new applications for business and personal lines and casualty insurance in California, USA TODAY reported.

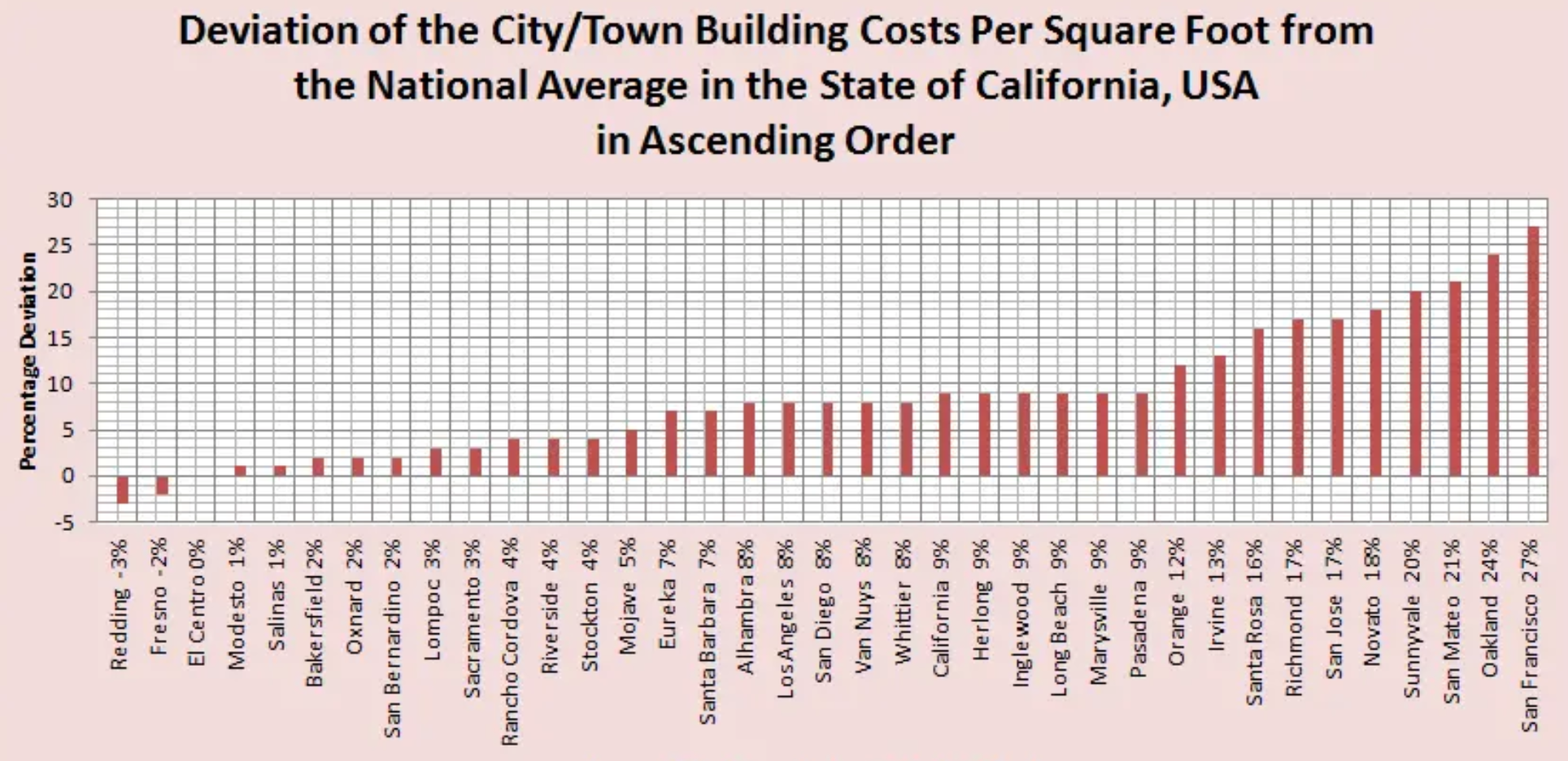

Building Cost Estimating, Construction, Outdoor Projects and Activities

State Farm said it will still work with the California Department of Insurance and lawmakers and will still serve existing customers.

The Oregonian reported that last year, California became the first state to require insurance premium discounts for those with wildfire protection safeguards at homes or businesses. That change was in response to soaring insurance costs for customers in high-risk areas.

“State Farm General Insurance Company made this decision due to historic increases in construction costs outpacing inflation, rapidly growing catastrophe exposure, and a challenging reinsurance market,” the company said in a statement.

CNN reported that scientists and California officials blame the climate crisis for the intensity of fire seasons. About 25 percent of the state’s forestland burned in the last 10 years — more than triple the previous decade.

The factors behind Illinois-based State Farm’s move are beyond the agency’s control, Michael Soller with the California Department of Insurance said. State Farm, with its affiliates, is the largest provider of auto and home insurance in the U.S.

I feel for you. I am a firefighter with 25 years and live in one of the most fire prone parts of the most fire prone states of Australia. State Farm will have made their decision simply based on actuarial number crunching to protect a bottom line and they are obliged to do that for their shareholders. That’s their duty. However, just pointing of the finger a yelling about climate change is very dangerous though. It means we can all – especially the authorites – look away from things like proper funding of forest and grassland management (planned burns, thinning programmes, construction and maintenance of breaks), the urban/forest interface through town planning, house design rules and more.

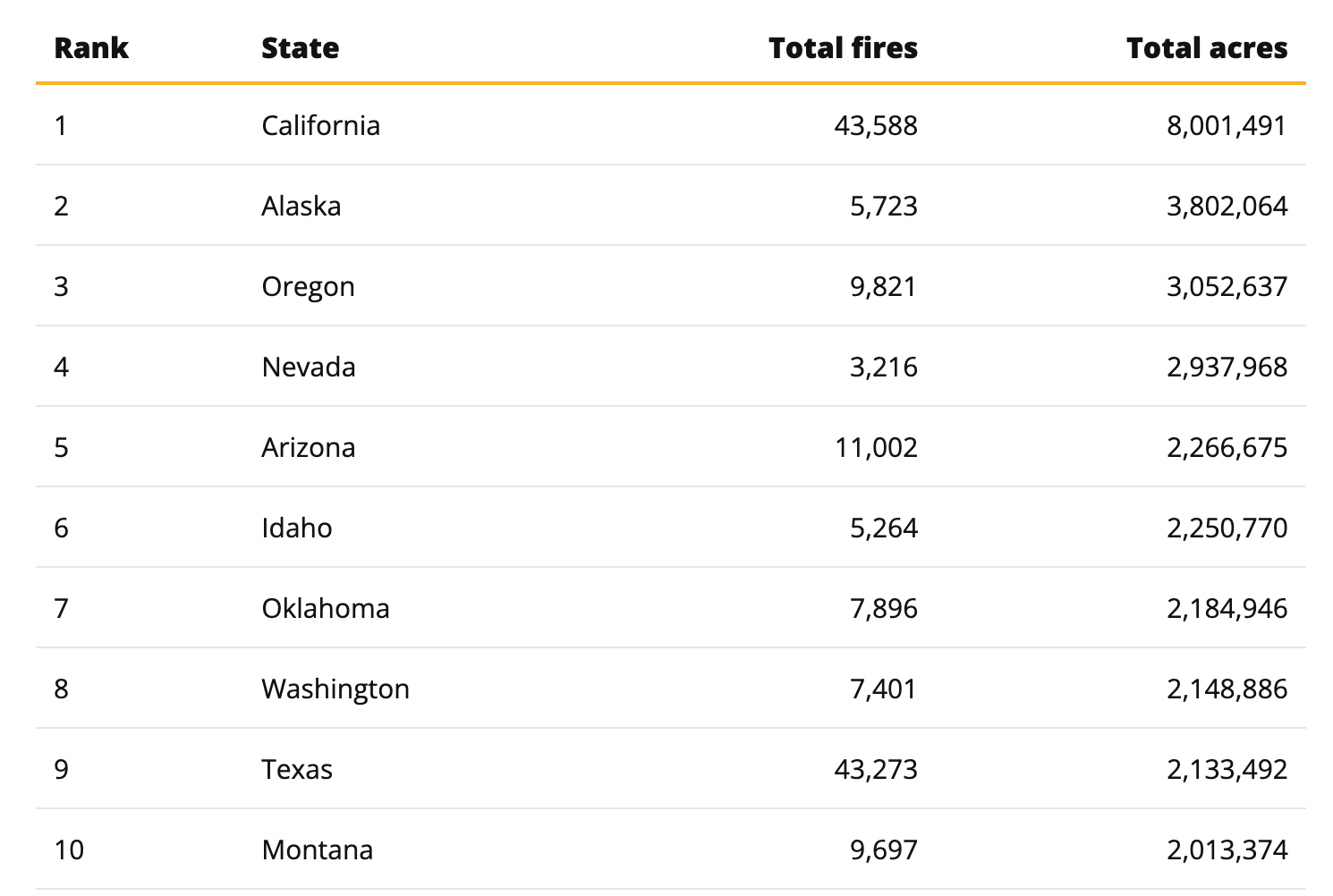

Let’s look at the statistics.

The article states “CNN reported that scientists and California officials blame the climate crisis” I find that hard to believe even if you accept that there is such a thing. The table in the article shows fire acerage by state plus number of fires and on the surface seems fairly straightforward but…California’s average fire size is only 184 acres. That’s tiny. Nevada is head and shoulders above that at 913 followed by Alaska at 664 and so on down the list, so something else must be at work. All states had to have experienced the same supposed “climate change” over the same time frame. So climate change is not the reason or they would all be uninsured. It’s just too easy a cop out. Looking quickly at the USA Census figures the big factor seems to be population density and here California beats all states on the list at 246 people per sq mile, followed by Washington at 104 and Texas at 101. None of the other listed states get over 60 per sq mile. As usual the answer to complex problems like this is never simple. There must be other factors too such as topography, fuel types and density, wind patterns during the fire danger period and so on, but a simple one size fits all answer is head in the sand stuff.

Love your work and look forward to your newsletters

Per that same table, California averages over 43,000 starts in a year. They get a large number of starts because of the population density you pointed out later in your post. They catch the overwhelming majority in the initial attack phase. When they don’t, they have the potential to consume a lot of acreage.

Texas has tons of starts, but gets excellent overnight recoveries, particularly in the eastern half of the state where I suspect the majority of their starts are (again, because of population density)

Agreed that California’s problems are complex and have numerous factors at play. Sometimes the media conflates climate and weather.

That doesn’t mean the climate isn’t growing hotter on balance. If you look at the change in global temperature alongside the growth in human caused carbon emmissions, it’s a fairly stunning correlation.

https://www.globalchange.gov/browse/multimedia/global-temperature-and-carbon-dioxide

Thanks for your respectful comment.

Cue Mike Stinson’s “The Late Great Golden State”

https://www.youtube.com/watch?v=Ow9FV3xjkew

Just one more reason to add to the already countless reasons to leave the Golden state………best to leave while you still can………

Just went through this with the renewal of my homeowner’s policy. Six months ago Mercury sent me a Google Earth photo of my house and a written demand to cut down two 107 year old trees or that were near my house, or risk having my insurance canceled. I had my independent agent shop my policy and he could not find anybody willing to write new business. They didn’t turn me down for risk factors, they simply weren’t accepting new customers.

So $3,500 later my two landmark trees have been cut down, the neighbors are pissed, I’m pissed, but I still have an insurance policy that will cover the catastrophic loss of my home in a fire, or so I hope. Don’t get me started on replacement values and code upgrade coverage….it’s truly a nightmare.

Mind you I’m not in a rural or urban/wildland interface area, my house is ten blocks from the beach in San Diego. My nearest exposure, a neighbor’s house, is 70 feet away. I’ve had zero claims in 35 years and I have other bundled policies with Mercury.

My agent said that insurance companies and the State of California are engaged in open warfare right now over rates. The insurance commissioner has not approved any new rate increases, so us homeowners are being held hostage in a giant game of chicken between the state government and insurance companies. The insurance companies have upped the ante by tightening underwriting criteria (in my case) or they’re leaving the state entirely.

My fear is that the state government’s new push to put every governing decision under the magnifying glass of equity (insurance for everybody regardless of their risk) will drive private insurance companies out and the state will then step in and be the only provider of fire insurance. In that case, nobody will win if there is no competition for our insurance premium dollar. Coverage will go down, prices will go up.

The State of California and insurance companies need to put their differences aside and enter into serious negotiations now to solve this impasse, or the citizens of California will suffer this coming fire season. Unfortunately however, we have a veto-proof supermajority one party legislature who are not motivated in the least to compromise.

No wonder people are leaving the state in droves.

Thanks for this comment on the article. I was struggling trying to explain why I thought State Farm’s decision is such a bad omen for homeowners, and it’s not simply because one insurer is opting out. Your take on Competition, the State offering Last Resort policies, and State Farm’s statement on rebuilding costs hit the mark. ( the article’s graph on construction costs seems way too low compared to what I’m understanding here in Colorado. Cali has to be way more out of line). The bottom line is that homes with little risk will be painted with a broad brush in terms of wildfire risk, and to a great deal, the costs of a policy are driven by ridiculous rebuilding costs, and the other parts of policies that pay rentals for 2 to 3 years while people wait to rebuild.

I think the companies that stay in will make a ton of money, and eventually start cutting each other’s throats on premiums, until it returns back down to earth. The insurance industry only makes money by selling policies, and only saves money by denying or delaying claims.

DOUG: [applause]