This is a portion of an article first published at Headwaters Economics in July, 2022. It is used with permission here.

Increasing home loss and growing risks require reevaluating the wildfire crisis as a home-ignition problem and not a wildland fire problem. A home’s building materials, design, and nearby landscaping influence its survival. Together with the location, arrangement, and placement of nearby homes, constructing a wildfire-resistant home is critical in light of rising wildfire risks. This report compares the cost of constructing a home to three different levels of wildfire resistance in California.

California is a leader in the country with a statewide building code and other property-level vegetation requirements addressing wildfire impacts to the built environment. Applicable to all new developments located in State Responsibility Areas (SRAs) and the highest fire severity zones in Local Responsibility Areas (LRAs), California’s Building Code Chapter 7A is intended to reduce the vulnerability of homes to wildfire.

Yet given the magnitude of California’s wildfire risks and increasing home development in wildfire-prone areas, constructing a home beyond Chapter 7A requirements may be needed to ensure greater wildfire resistance. Understanding the comparative costs of wildfire-resistant home construction in California can inform future wildfire policy and decision-making.

This report compares the costs for constructing three different versions of a wildfire-resistant home in California:

- Baseline home compliant with the minimum requirements of Building Code Chapter 7A;

- Enhanced home augmenting Chapter 7A requirements with a vertical under-deck enclosure around the perimeter of the deck and a noncombustible zone around the home (0 to 5 feet), including under the deck and extending five feet out from the deck perimeter; and,

- Optimum home constructed to the most stringent, fire-resistant options (e.g., use of a noncombustible material), or in some cases, a “Code plus” option (an option not currently included in Chapter 7A). Optimum performance levels were selected based on recent research findings and best judgment.

Building materials and assemblies for five primary home components were considered, including:

- Roof – roof covering, vents, roof edge, and gutters (including gutter covers and drip edge)

- Under-eave area – eaves, soffit, and vents

- Exterior wall – siding, windows, doors, trim, and vents

- Attached deck – horizontal surface area, rails, and under-the-deck footprint

- Near-home landscaping – the immediate five-foot perimeter around the home and attached deck (including mulch and fencing)

Cost estimates for individual building materials were provided through RSMeans, a national database of construction costs for residential, commercial, and industrial construction. Cost estimates included building material, labor, equipment, and contractor overhead costs such as transportation and storage fees.

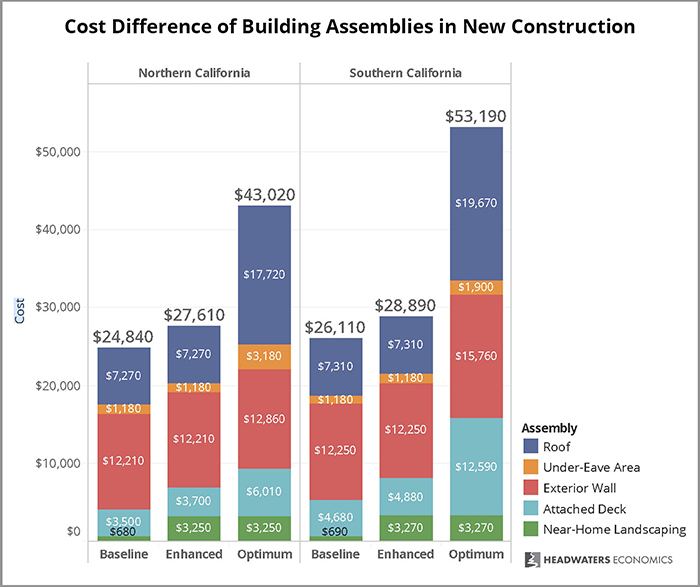

In northern and southern California, building an Enhanced wildfire-resistant home increased construction costs by approximately $2,800 over the Baseline home. Constructing a home to Optimum wildfire resistance increased overall costs by $18,200 in northern California and by $27,100 in southern California.

Although the Optimum home was more expensive to build, it is likely that the increased costs will return greater long-term benefits in energy efficiency and durability. The roof, exterior walls, and near-home landscaping added the largest proportional increases to building costs. Each of the five components is described in more detail below.

Read the entire article at Headwaters Economics.